The illusion of inclusion and the financial health crisis

On the surface, Kenya is the global poster child for financial inclusion, particularly as driven by digital payments. The 2024 FinAccess Household Survey reports an 84.8% formal inclusion rate, up from 83.7% in 2021. But a critical distinction is becoming harder to ignore: having an account does not automatically translate to financial health.

Financial health goes beyond access reflecting a household’s ability to absorb shocks, maintain consumption, and recover without falling into distress. While technological innovation has closed many access gaps, it has not necessarily made households more resilient.

The infrastructure of inclusion is now largely in place. But the 2026 Tala MoneyMarch report suggests that the financial health of the average Kenyan is under pressure. An overwhelming 89% of consumers, up 3 percentage points from 2025 report that rising costs are affecting their household budgets.

This pressure is not just about inflation. It is also about unstable income and business uncertainty. As essential spending rises, households are cutting back on savings and discretionary spending. In this environment, digital credit has become a critical coping tool that is fast, accessible, and often the first place people turn in moments of need.

But while digital credit solves for access, it raises a more important question: what is it actually doing for financial stability?

Borrowing to Survive, Not to Thrive

There has been a clear shift in how credit is being used within Kenyan households. Traditionally, credit functioned as a tool for building assets, expanding businesses, and enabling upward mobility. Today, it increasingly acts as an emergency liquidity tool, helping households bridge short-term gaps.

Borrowing to cover day-to-day needs has surged to 47% in 2026, up from 36% just a year prior.

Credit used for business restocking has dropped from 35% to 24%.

46% of consumers now use loans to supplement their income.

For many households, debt is more reactive than strategic. It helps to address immediate needs but often masks deeper financial strain. This shift from ‘thrive’ to ‘survive’ is subtle but significant. It suggests that credit is no longer primarily enabling growth but is increasingly substituting for unstable income.

The Resilience Gap

In financial inclusion, resilience is often measured by how quickly a household can recover from a shock. But for many Kenyans, there is very little buffer to begin with.

24% of households would survive for less than one month if their income disappeared.

While 76% of Kenyans report having some emergency funds, only 59% have at least one month of coverage.

Digital credit has become the default shock absorber. Around half of consumers turn to digital loans in emergencies, largely because funds can be accessed within 48 hours. But this raises a deeper issue on the use of credit to absorb shocks, rather than recover from them, which results in managing instability rather than building resilience. This financial challenge is not just structural. It is also behavioral, shaping how households think about the future and make financial decisions.

The behavioral and structural risks

89% of households indicate that the rising costs of essentials is a primary driver of financial strain meaning the future becomes harder to prioritize. One of the clearest signals of this shift is the growing pressure on the youth.

75% of people aged 18–34 have postponed or abandoned long-term goals

5% believe those goals are permanently out of reach

This is more than a short-term adjustment. It is a reallocation of resources away from investment in necessities such as education, housing, business, and more toward immediate survival. Over time, this has real consequences. Less investment today means lower asset accumulation, weaker income growth, and reduced economic mobility in the future.

The entrepreneurial trap: Survival disguised as opportunity

Kenyans are adapting but not always in ways that build long-term stability. The rise in entrepreneurship, ‘hustle’ is, in many cases, a response to pressure rather than opportunity. As formal employment becomes less reliable, more people are turning to business ownership as a way to survive. While this looks like resilience, it is often a high risk trade off.

Many of these businesses are:

Undercapitalized

Highly exposed to market shocks

Dependent on the same strained customer base

At the same time, side hustles are giving way to full-time, necessity-driven entrepreneurship. Instead of diversifying income, people are concentrating risk into a single, often fragile, source of income. This creates what we might call an entrepreneurial trap reflected by people moving into business ownership to escape income instability, only to face even greater uncertainty. This uncertainty is reflected in the statistics with estimates suggesting that around half of SMEs in Kenya don’t make it past their first three years, and in some cases, as many as three out of five businesses close within just two years.

In that context, the rise in necessity-driven entrepreneurship takes on a different meaning. If many of these businesses are inherently unstable, and households depend on them for income, then digital credit, in addition to supporting individuals, is helping to sustain businesses that are already in crisis. Instead of enabling growth, credit can end up keeping both the business and the household in a constant cycle of just getting by.

Re- imagining digital lending as a tool for resilience

For digital credit to play a meaningful role from a coping mechanism to a resilience tool, its design must evolve. At the moment, it provides fast on demand liquidity in moments of crisis. But resilience is not just about surviving the shock but about what happens after access.

Do households recover? Do they stabilize? Or do they continue borrowing just to stay afloat?

Answering these questions requires rethinking what digital credit is designed to do.

From emergency liquidity to financial stability

Most digital credit today is reactive. A shock happens, and credit fills the gap.There is an opportunity to shift toward more predictive models where households have access to buffers before they reach crisis point. This could include:

Pre-approved emergency limits

Credit triggered by income patterns

Products designed around predictable expenses like school fees

One of the biggest missed opportunities is that credit is often disconnected from how people actually earn. For many Kenyans, income is irregular and unpredictable. Fixed repayment structures can create additional stress, increasing the risk of over-indebtedness. A more effective approach is to align credit with real cash flows by embedding it into livelihoods. This means linking access and repayment directly to how income is generated, whether through mobile money transactions, supply chains, or daily business activity.

But we cannot expect credit to move financial health in isolation. There is a need to strengthen the connection to the rest of an individual’s financial life, specifically, savings and risk protection. Here, simple design shifts could make a meaningful difference:

Setting aside small savings during repayment

Creating dedicated emergency wallets

Bundling credit with insurance

These can fundamentally change the role of credit from a short-term fix to part of a longer-term safety net.

Create pathways out of dependency

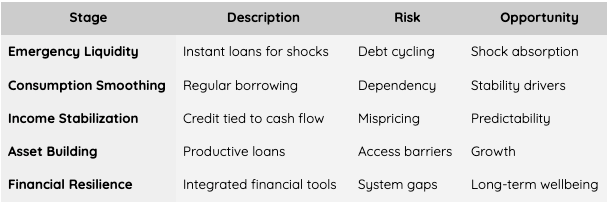

Finally, resilience requires progression. At the moment, too many users remain stuck in cycles of small, short-term loans. What’s missing are clear pathways that allow borrowers to graduate:

From emergency loans to working capital

From consumption to investment

From survival to stability

The Digital Credit to Resilience Pathway

Without this progression, digital credit risks becoming a tool that simply maintains transaction activity but doesn’t meaningfully improve outcomes.

Designing for Resilience, Not Just Access

Kenya’s financial inclusion story is a success, if that was all that is needed for financial health. Many households are not using credit to move forward, but to stay afloat. Digital credit has become a critical shock absorber but it is often compensating for unstable incomes rather than strengthening them.

Closing this resilience gap will require more intentional credit design: products aligned to real income patterns, better use of data to detect financial stress early, and stronger links between credit, savings, and income generation. It will also require a shift in how success is measured, not by how quickly loans are disbursed, but by whether they improve stability over time.

This shift is becoming more urgent as deeper risks emerge. Young people are delaying long-term investments, shaping future economic mobility. Necessity-driven entrepreneurship is rising, often without the stability needed to sustain growth. And climate-related shocks are adding new layers of financial pressure.

The question for the next phase of financial inclusion is simple but critical: are we building systems that help people recover and grow, or simply making it easier to manage decline?

At Tola Group, we focus not just on expanding access, but on understanding what that access actually delivers and the impact on livelihoods. Working across digital financial ecosystems, we see how tools like credit function in people’s daily lives. What this points to is a clear shift in focus for the sector: from increasing access to ensuring that access translates into real financial stability and resilience of livelihoods.

In the next blog in this series, we move from diagnosis to design exploring what it will take to turn digital credit into a tool that actively builds financial resilience. We will look at how credit can be embedded into livelihoods, what more intentional product design looks like in practice, and where development partners can play a catalytic role in shaping better outcomes.